.webp)

Podcast

Market Insights for June 2026

Market Insights for June 2026

Listen to this episode and subscribe on your preferred podcast platform:

*Sign up for our Q2 Equipment Market webinar on June 24 for a deeper dive into these categories and more. Andy Campbell frames up the first half of 2026 with a category-by-category look at used equipment trends — and a recurring theme: inventory is improving, but sales velocity is not keeping pace.

Andy Campbell covers four converging stories shaping the equipment market as the first half of 2026 wraps up: Deere's Q2 earnings, a tariff reduction, a sharp commodity sell-off, and used equipment signals that are stabilizing in most categories — but not all.

Deere Q2 Earnings: Construction Carries the Load

Deere reported $13.4B in Q2 revenue (up 5% YoY), beating analyst estimates with $6.55 EPS vs. $5.70 expected. But the segment split tells the real story:

- Production & precision ag: Revenue down 14%, operating profit down 39%

- Small ag & turf: Revenue up 16%, operating profit up 25%

- Construction & forestry: Revenue up ~30%, operating profit up ~50% — driven by infrastructure spending, data center build-out, and road construction

- Management reaffirmed FY2026 as the cycle bottom; U.S./Canada large ag volumes expected down 15–20% for the full year

- Deere received ~$250M from IEEPA tariff refunds — a one-time margin boost, not structural relief

Tariff Shift: Ag Equipment Drops to 15%

President Trump signed a proclamation on June 2nd cutting tariffs on imported ag equipment from 25% to 15%, effective June 8th through end of 2027.

- Some margin relief for OEMs, but don't expect lower sticker prices near-term

- New equipment pricing still likely to rise 1–6% through end of 2026 — just potentially a point lower than before

- Experts project large ag industry stabilization in H2 2026 as deferred purchases begin cycling back

Commodities: Corn Takes a Hit

July corn futures dropped to $4.19/bushel — down nearly 30 cents in a single week and the lowest since October 2025. November beans fell to $11.15–$11.35, the lowest since April 2025.

- Near-ideal planting conditions and rain are boosting yield expectations, removing risk premium

- Managed money has aggressively liquidated long positions; more selling likely

- No Chinese demand materializing on beans — a meaningful demand miss

- The Purdue/CME Ag Economy Barometer fell to 119 in May; the Farm Capital Investment Index hit its lowest since September 2024

- 51% of farmers cite high input costs as their top concern — a survey record

- Next key date: July WASDE report for updated ending stocks and planted acreage

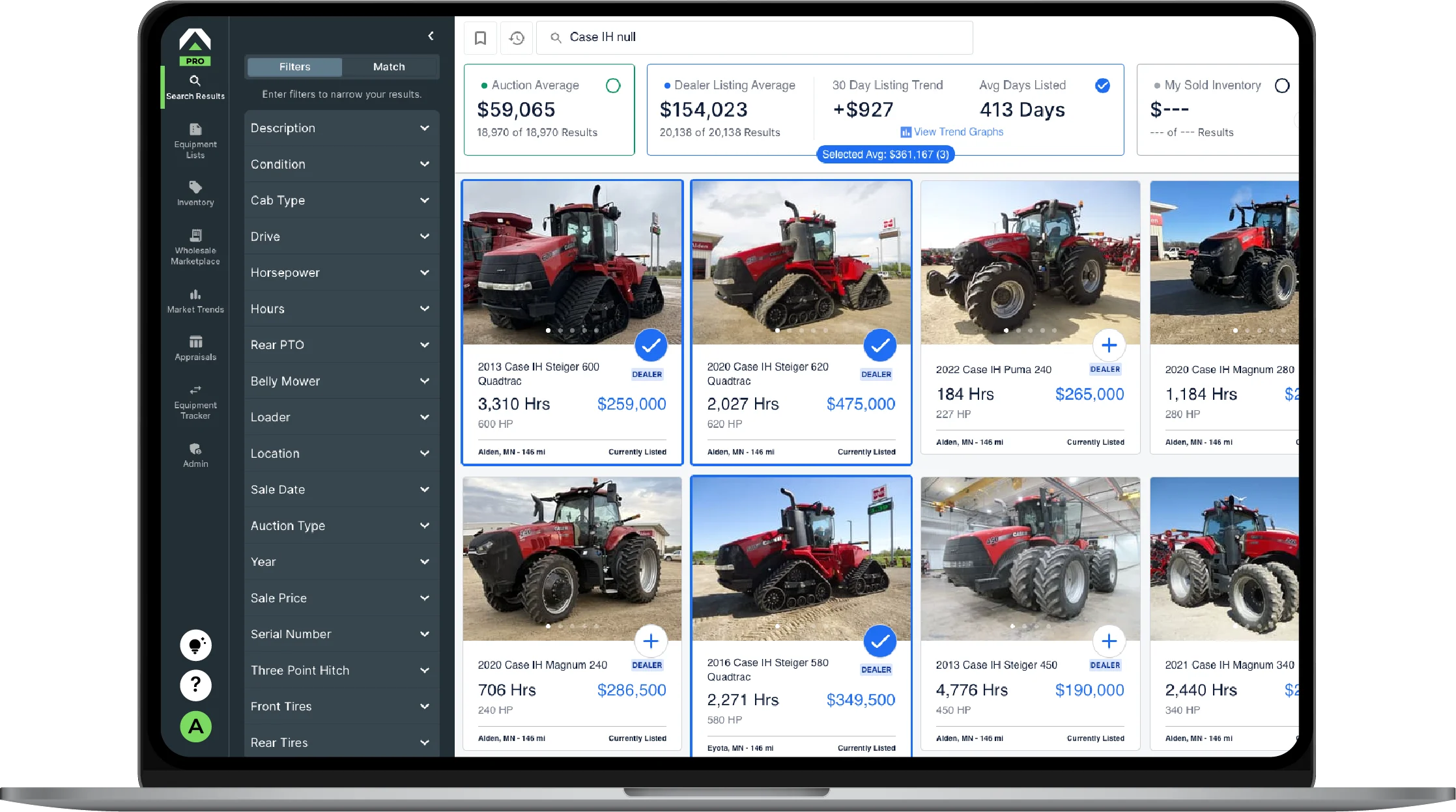

Used Equipment: Stabilizing, With Exceptions

Compact tractor inventory down 8% month over month (30% YoY). Planter supply continues to draw down. Some auction values are ticking up, especially on low-hour equipment, as price-averse buyers shift from dealerships to auctions.

- Grain carts remain a concern: Days on lot climbed from ~300 to 400+; asking prices up ~13% YoY. Farmers are treating grain carts as elastic, deferrable purchases — and that behavior could spread to headers, four-wheel drives, and eventually row crop tractors.

- Row crop tractors and combines: sales still near the bottom. May data isn't definitive, but early June auction activity should set the tone for summer.

Sources

More Podcasts from Beyond the Hood

Inside Tractor Zoom With Hank Mandsager

Market Insights for July 2026

Closing the Technician Gap with AI: John Schmeiser of VisorPro

Join the future of ag & heavy equipment sales

Take a guided tour of Tractor Zoom Pro and Anvil Pro to discover how wider margins and faster turns are just a few clicks away.