.webp)

Podcast

Equipment Trends for July 2026

Equipment Trends for July 2026

Listen to this episode and subscribe on your preferred podcast platform:

Andy Campbell digs into four equipment stories for July — combines, utility tractors,planters, and direct dealer feedback — with a recurring theme: the mood is running ahead of what the category-level data actually shows.

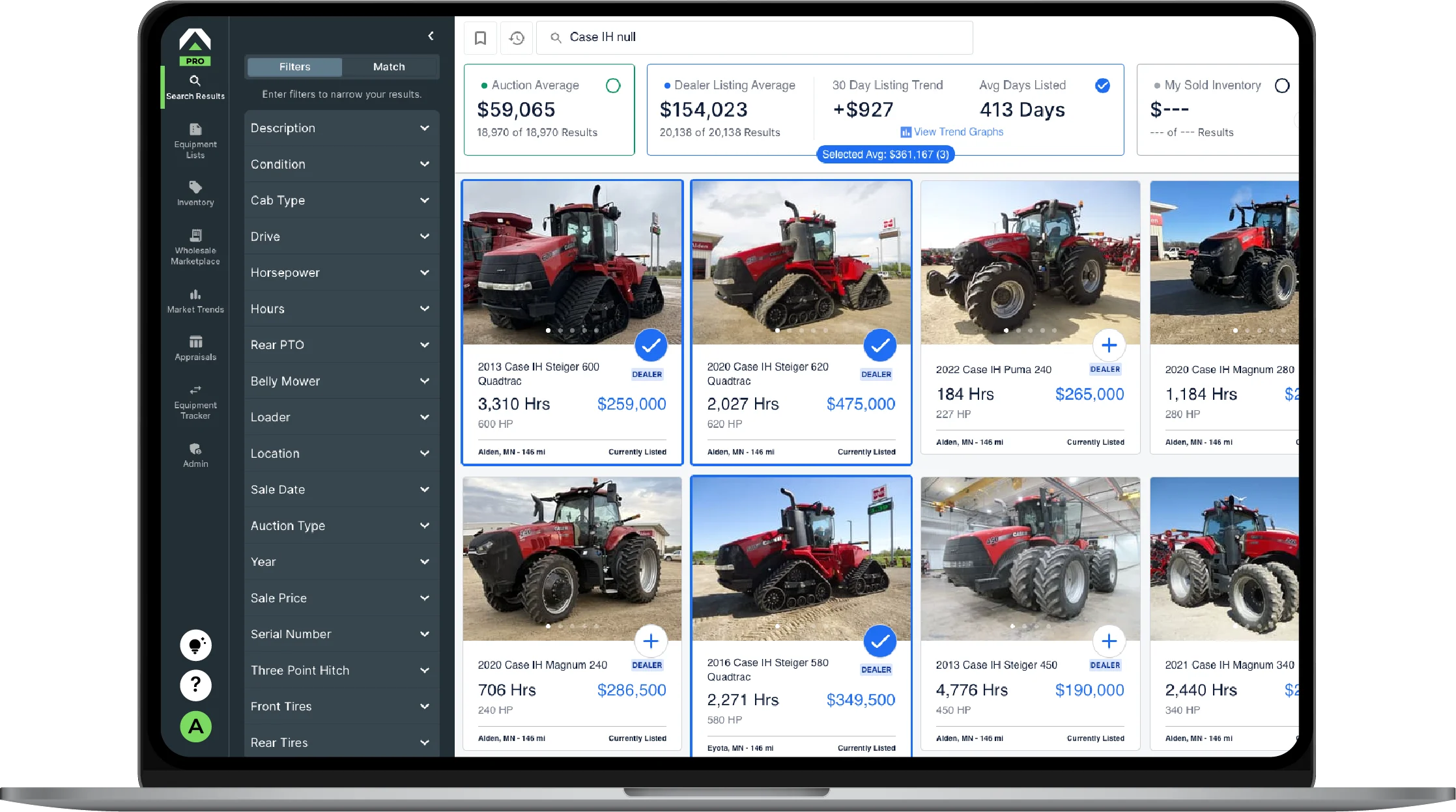

Combines: Class 8s holding, 9s and 10s are the real risk

66% of dealers named combines their top concern in Tractor Zoom's June 24th webinar poll. But the class 8 data tells a more nuanced story:

- Class 8 supply down ~16% YoY, down 37% from the August 2024 peak

- Recent sold values on 780s and CNH 8250s have beaten both 2024 and 2025 spring levels

- Class 9s and 10s are where risk concentrates — supply hasn't drawn down nearly as much, and the second-owner market remains an open question

- July and August are the pivotal window to move combines before the next opportunity in November/December

Utility tractors: Bright spot with an aging cliff ahead

Supply is down 30% YoY and auction values are running 5–10% stronger than last year. But the last five months have been flat, and a large volume of inventory sitting at 90–270 days on lot will start crossing the 360-day "aged" threshold starting in August.

- If summer sales don't materialize, aged utility tractor inventory will jump significantly before year-end

- Cattle market headwinds are emerging — non-cow-calf producers are stretched between equipment and high calf prices

- Act now: assess your inventory, pending inventory, and aged position and plan through end of summer

Planters: Early signs of resurgence

Supply down ~37% YoY, 50% off 2024 highs. The standout signal: 22% of June inventory was 0–30 days old — a clear trade-in restocking bump tied to the Deere early order period.

- Dealers are reporting better-than-expected early order periods — the best in nearly three years

- Planters were the first category into this correction and may be the first showing a real demand recovery

- Combines could follow a similar pattern as buyers replenish aging fleets this summer

What dealers are telling us

Direct conversations and webinar feedback are surfacing several patterns:

- $100K–$150K weakness: A spending range that's showing softness that wasn't there a year ago — more research underway

- Vertical tillage: Some dealers calling it "dead and saturated." Strip-till/no-till adoption plus high fuel costs are reducing pass frequency

- 8R buildup: Increasing inventory accumulation, particularly in eastern markets

- Pre-DEF tractors under 5,000 hours: Still unicorns in the sub-$150K range

- Folding row crop headers (especially 12-row): Sitting longer; platform headers down 20–30% in supply with strong brand premiums (MacDon FD70 vs. Case IH 2162 case study coming)

Sources

- Purdue/CME Group Ag Economy Barometer — May 2026 (Farm Capital Investment Index at 41, lowest since September 2024)

More Podcasts from Beyond the Hood

Inside Tractor Zoom With Tyler Lowy

Market Insights for June 2026

Building Stronger Dealerships from the OEM Side: A Conversation with CNH's Brian Weaver

Join the future of ag & heavy equipment sales

Take a guided tour of Tractor Zoom Pro and Anvil Pro to discover how wider margins and faster turns are just a few clicks away.