.webp)

May 2025 Ag Equipment Market Trends: 5 Key Insights

As the 2025 planting season continues, a series of economic, financial, and policy shifts are beginning to influence the U.S. ag equipment market and shape how farmers invest and how equipment supply is expected to evolve. Below are five key takeaways for understanding where the ag economy stands and how it's impacting equipment demand and valuations.

For more information on these macroeconomic factors and how they are impacting equipment dealerships, sign up for our newsletter or watch the latest episode of Trends in 10 with Tractor Zoom’s Director of Insights, Andy Campbell.

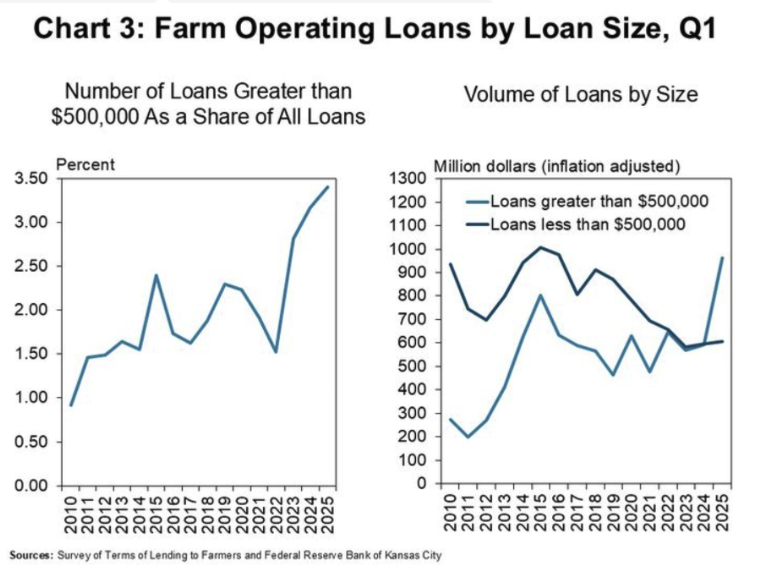

Source: Kansas City Federal Reserve Bank

1. Rising operating costs and farm loan sizes signal financial pressure

New data from the Kansas City Federal Reserve reveals a notable rise in non-real estate farm loan volume, particularly loans over $500,000, which now make up a record 3.5% of all loans tracked since 2010. This growth reflects the increasing cost of doing business for farmers, driven by elevated land values, expensive inputs, and large equipment purchases.

Operating loans have risen for six consecutive quarters, reversing a downward trend that began in 2022. The higher cost of capital (especially when borrowing for newer, high-ticket machinery) is pushing more farmers to look for more favorable financing options.

2. Signs of correction: Land and equipment values rebalancing

U.S. farmland values have begun to decline year over year for the first time in nearly a decade. While the correction is mild compared to the 1980s farm crisis, early comparisons show that farmland tends to take longer to adjust than equipment markets. In fact, a noticeable correction in used equipment values has been underway for roughly 18 months.

Collateral requirements from lenders have also returned to pre-COVID levels, another sign that credit conditions are tightening. As financing standards revert to late-2010s norms, equipment dealers may encounter customers who are more cautious and dependent on accurate, defensible valuations.

3. Commodity outlook mixed: Corn faces oversupply risk

The outlook for commodity markets is mixed, especially for corn. With 95.3 million acres planted and a projected yield of 181 bushels per acre, the U.S. could produce a record corn crop. If realized, this would likely suppress corn prices and weigh on farm profitability. However, weather remains a wild card. A significant drought could reverse these expectations and drive prices up.

This uncertainty may contribute to uneven regional equipment demand: stronger in drought-impacted zones if prices rally, but weak in areas where crop profitability lags. Overall, dealers should prepare for regional variability in buying behavior through summer and fall.

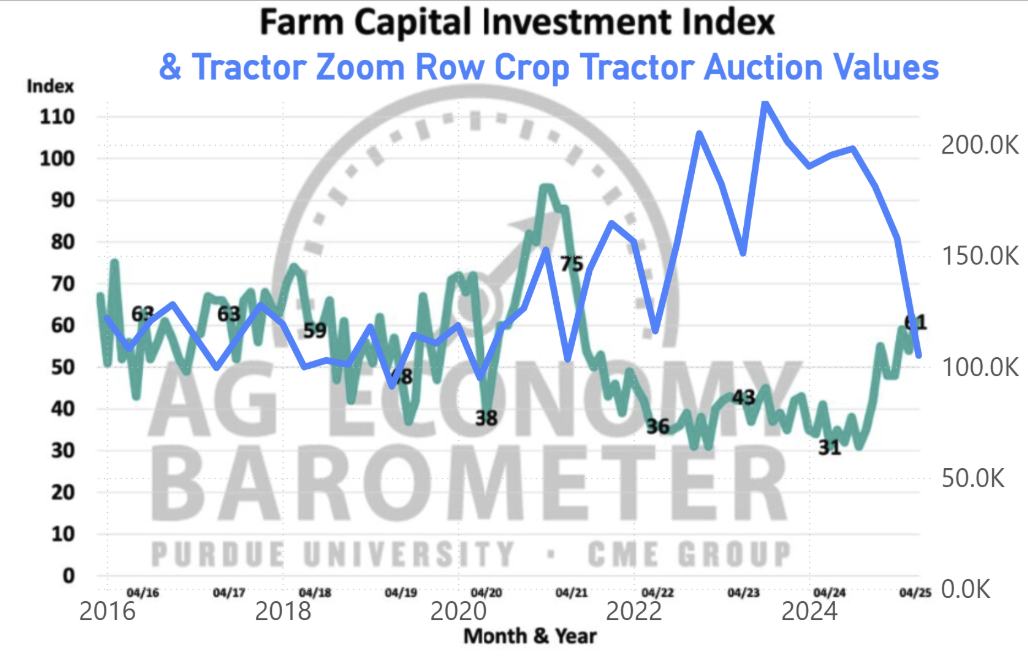

Source: Purdue University and Tractor Zoom Pro’s Market Trends data

4. Return to a "new normal" for used equipment

After several years of volatility, used equipment values appear to be stabilizing. Purdue’s Farm Capital Investment Index rose to around 60 in April—its highest reading since early 2020. The index’s rebound comes alongside greater equipment availability and lower inflationary pressure on prices.

Auction values for row crop tractors and 400+ horsepower machines have already dropped roughly 11% year over year. Supply for this category is up 38%, and more trade-ins are expected through the summer. Without a commodity rally, this segment will likely remain under value pressure through at least the end of Q3.

In contrast, Class 8 combine inventories have stabilized. Supply increased only 3% year over year, reflecting effective dealer management. Values this spring are lower than last year’s peak but are trending above late-summer 2024 levels. If dealer inventories remain in check, combine values could perform better through the remainder of 2025—even with muted corn profitability.

5. Policy shifts and market forces to watch

A few key policy developments may affect long-term demand. The 45Z biofuel blending tax credit passed through the House Ways and Means Committee, signaling future support for ethanol demand. However, the Iowa Senate’s move to block carbon pipeline projects through eminent domain may hinder efforts to make ethanol viable for sustainable aviation fuel (SAF)—a potential growth area for corn demand.

Meanwhile, lingering supply chain vulnerabilities could re-emerge later this summer, particularly if new tariffs disrupt global manufacturing. If this occurs, it may put upward pressure on used equipment values in late 2025 or early 2026 as farmers shift away from new purchases.

Final takeaway: Dealers need to prepare for this new normal

From rising capital costs to evolving policy landscapes and regional crop variability, the ag equipment market is facing a period of recalibration. While a full-blown correction remains unlikely, evidence points to a “new normal” defined by stable (but not stagnant) values, more conservative lending behavior, and slower capital investment.

Dealers and lenders alike should keep a close eye on weather, inventory movement, and credit trends in the coming months. Using real-time valuation data tools like Tractor Zoom Pro’s Equipment Market Trends is one way to ensure your dealership stays on top of crucial pricing patterns and is informed to make the right inventory adjustments to keep your dealership competitive in times of uncertainty.

Join the future of ag & heavy equipment sales

Take a guided tour of Tractor Zoom Pro and Anvil Pro to discover how wider margins and faster turns are just a few clicks away.