.webp)

2025 Year-End Equipment Market Summary & Key Trends in 2026

As 2025 closes, the used equipment market is resetting in ways that will matter for every dealer and lender heading into the new year. Supply constraints from the post-pandemic period have eased, yet demand is softening faster. This has been driven by tighter margins, lower commodity prices, and more cautious spending across farms and businesses.

These shifts are of course not happening evenly. Some segments are stabilizing, while others are facing accelerated aging, slower movement, or widening value gaps between retail and auction.

Key takeaways from the 2025 EOY Market Report

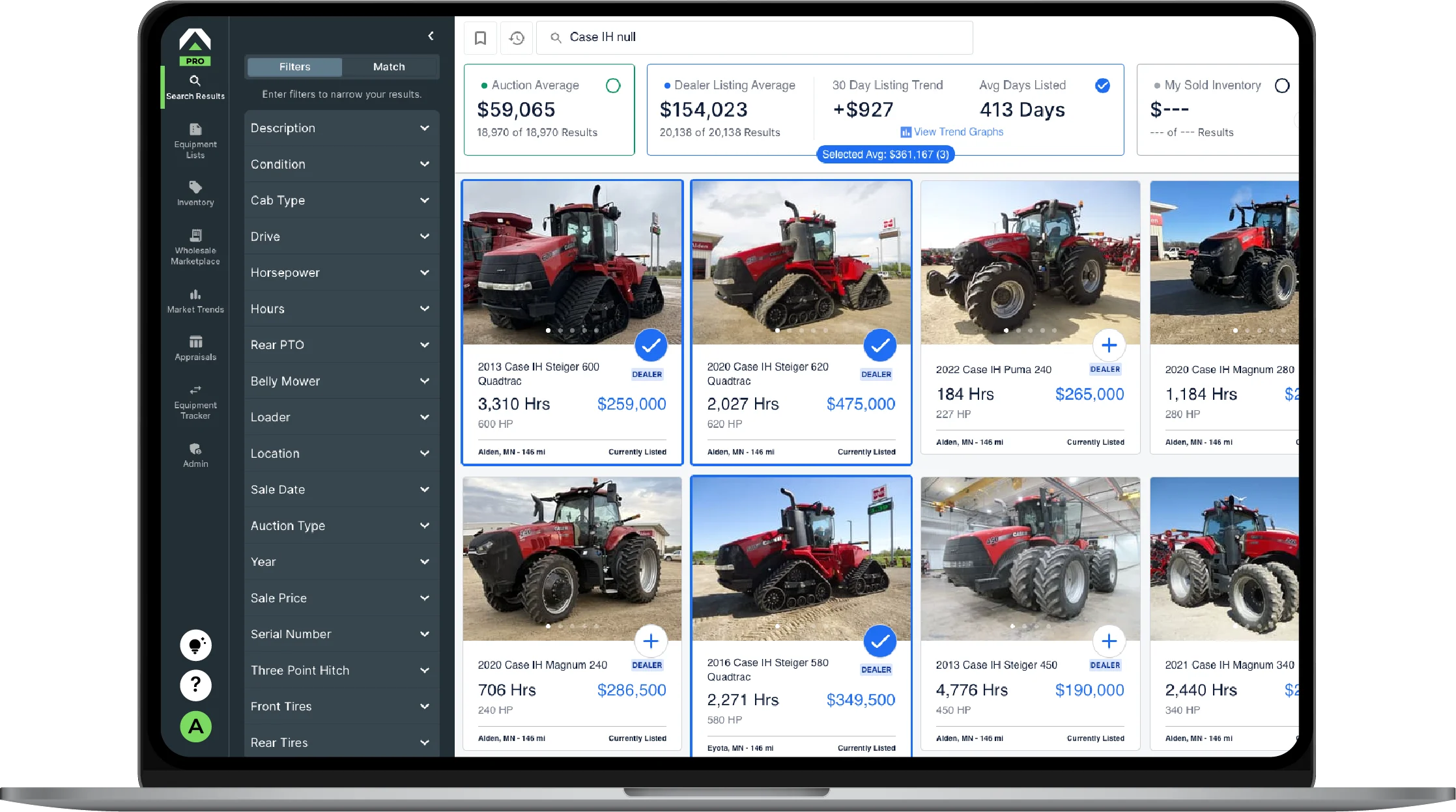

Here’s a quick look at the major patterns by category that are shaping the market as we enter 2026, all retrieved from Tractor Zoom Pro's equipment valuation database. Download the full report to dig deeper.

1. Tractor categories moved in opposite directions.

Compact tractors saw slower sales and rising aged inventory, while utility tractors remained one of the few segments with stable demand and improving late-year turns.

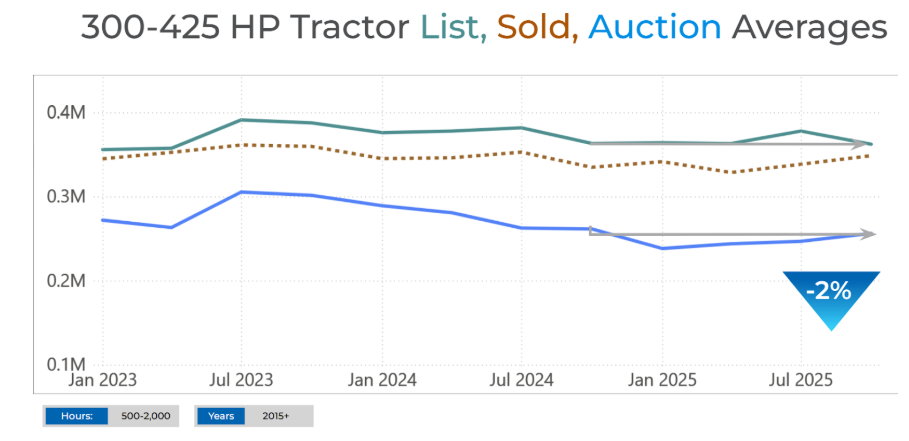

2. Row crop and 4WD tractors continue to soften.

Even with inventory trending lower, demand fell more sharply—pushing turns down, aging up, and keeping late-year pricing under pressure.

3. Combines show a split market.

Class 8 combines are stabilizing, but Class 9+ models face oversupply, elevated aging, and widening retail-to-auction price gaps heading into 2026.

4. Planters and sprayers remain high-risk categories.

Planters experienced some of the steepest demand declines of the year, while sprayers held value but saw aging intensify, especially for older units.

5. Buyers remain selective, favoring newer, low-hour equipment.

Across categories, newer units continue to move while aging inventory remains the biggest drag on turns and margins. The market is rewarding strong specs, low hours, and clean condition.

What this means heading into 2026

For dealers, the greatest risk heading into 2026 is aging, not availability. Markets are moving more slowly, and buyers are more cautious, meaning the timing of acquisitions, pricing discipline, and exit strategies will matter more than ever.

For lenders, equipment now represents a larger share of farm balance sheets than before the pandemic. As values flatten or soften in several categories, portfolio risk depends heavily on understanding which segments and machines carry the most exposure.

The data is clear: success in 2026 will depend on real-time visibility, disciplined inventory management, and spec-level insight into where values are holding, softening, or diverging.

Join the future of ag & heavy equipment sales

Take a guided tour of Tractor Zoom Pro and Anvil Pro to discover how wider margins and faster turns are just a few clicks away.