Swelling Self-Propelled Sprayer Volume

Like other categories of equipment, sans combines last fall, the rising supply of self-propelled sprayers is catching the eye of most in the ag industry, but so far hasn't caught too many off guard. In this analysis I'll walk through the rate of supply increase that we've seen for these applicators and how the price has responded. If listening is more your style, you can play the recording below that talks through this same analysis.

If you want to delve further into this and other categories, we'll be holding an an equipment market update webinar in November. You can register for that now here.

https://www.youtube.com/embed/Wbd6Oh4_-ro?si=KiXJTPLKnhHCHluB

For those who prefer reading, here you go:

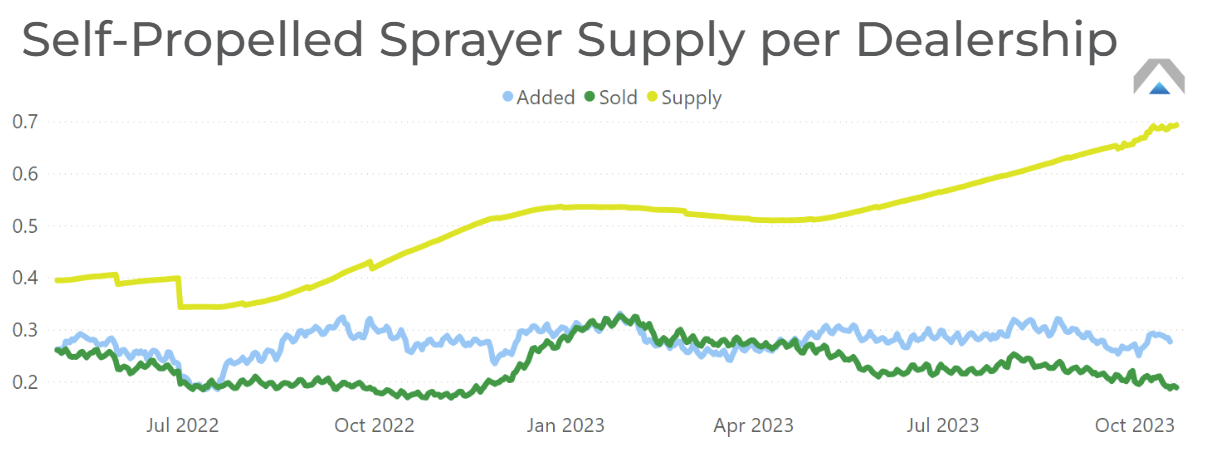

The return of supply has not been evenly distributed amongst equipment categories. Compact tractors were easy for many manufacturers to create and distribute. Combines were needed for fall harvest, albeit late to the party, creating a backlog of machines were are currently working through. Larger, non-4WD tractors followed and continue to make their way down the highways. Now it is sprayer's turn, and we are seeing that supply increase 50% over the levels this time last year.

Peak Sales Season for Sprayers

Sprayers' peak sales season is just around the corner. Right after harvest up until planting season is peak time to move these applicators. This past year the sales season ran into a headwind of uncertain profitability and higher interest rates, so while supply plateaued for half the year, it didn't retract. Now with new supply coming into the market, many are watching the external market to anticipate farmers' demand.

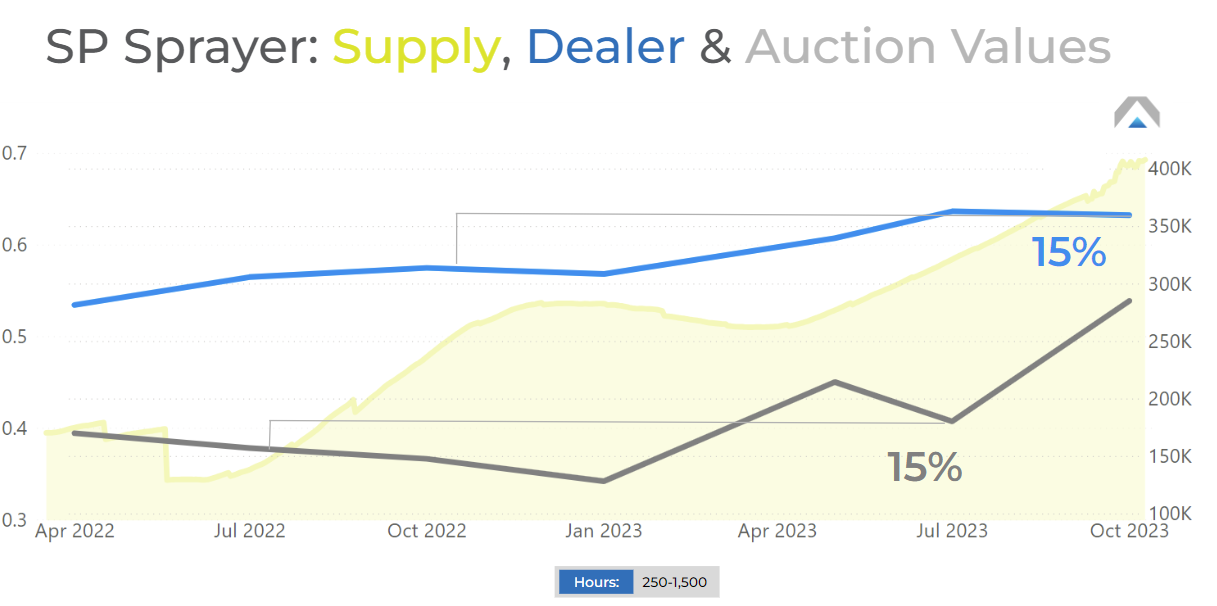

In addition to farmers' purchasing power being a drag on sales will be how much further those dollars need to stretch this year. While combines and tractors, to a lesser extent, have pulled back on their retail and auction values, sprayer values continue to rise. This is occurring both on the dealer lots and auction.

In the graph above you can see that the rising supply is not negatively affecting values. Yet. In next month's webinar, we'll review a few other categories of equipment where this is not the case. Here though, the demand remains strong enough to still support the more-sensitive auction values.

Another explanation to the supporting demand is that the make-up of what is on lots and at auction is changing. There are two sides to every coin and the painful reality of the last couple years of high farm profitability is that many 'second buyers' who would normally purchase a slightly used machine, bumped up and bought new. Now this is appearing to create a larger subset of those second-tier, once-used machines. Throw in a significant price increase and what once cost an average of $375K to purchase a 1-2 year old sprayer with 500-1,000 hours on it in 2021, now is going for an average of $442K, at a significantly higher interest rate.

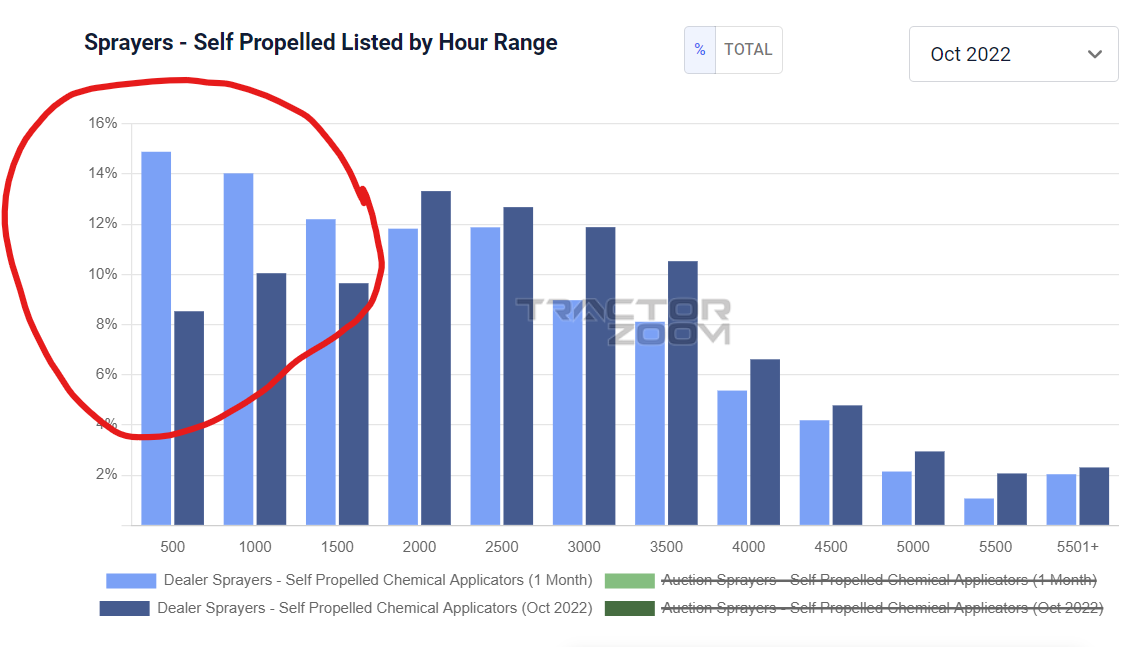

In the graph above you can see the dramatic shift from last year's supply (dark blue) to this current supply (light blue). About 42% of available supply has less than 1,500 hours on it, whereas last year that same segment comprised of only 28% of available inventory. This is by no means a 'sky-is-falling' scenario, but rather one that might require a shift in strategy and close attention to your sprayer inventory now that you are aware of it.

We'll cover this more in-depth for more categories in next month's webinar. Remember, if you have not signed up yet, you can do so below.

Join the future of ag & heavy equipment sales

Take a guided tour of Tractor Zoom Pro and Anvil Pro to discover how wider margins and faster turns are just a few clicks away.